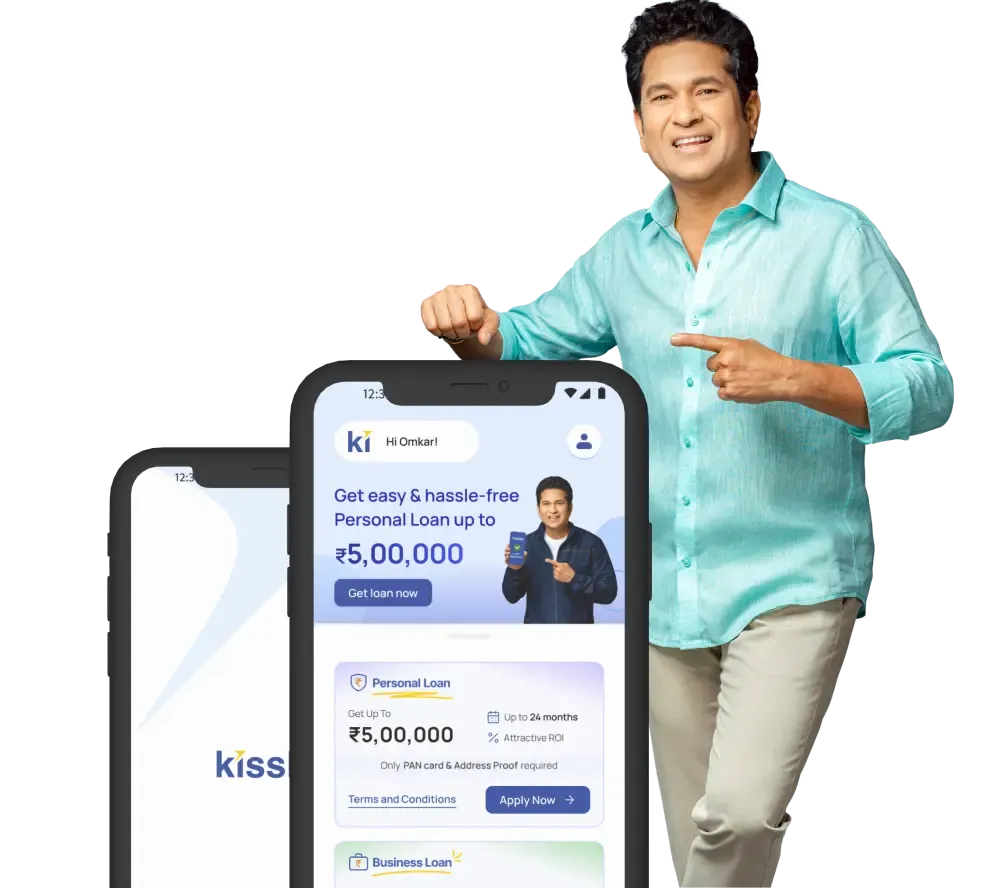

Free Credit Score Check-

Speedy & Safe

Get your Credit report Instantly in minutes

Powered byWhat is credit score?

Your credit score is like a financial report that shows lenders how well you manage money. Expressed as a three-digit number, usually between 300 and 900, it reflects your repayment habits, loans, and credit usage.

A higher credit score enhances your chances of securing approvals on loans and cards at better terms. With a quick credit score check, you can understand where you stand financially.

At Kissht, we help you check your credit score for free, so you can stay financially prepared and loan-ready whenever opportunities arise.

Why is credit score important?

Think of your credit score as the trust signal that banks and lenders use before saying “YES” to your loan or card request. It’s like your financial reputation wrapped in numbers. A quick credit score check tells you how reliable you appear in repaying money.

The importance of credit score lies in the doors it opens—better approvals, lower rates, and higher limits. Today, anyone can check their credit score for free online, making it easier to track and improve. Simply put, a good credit score is your ticket to smoother financial opportunities.

How does credit score work?

First, enter your mobile number

OTP verification

Enter your basic details

Get your credit score for free

Benefits of regular credit score check

Stay loan-ready anytime, anywhere instantly

Spot errors early, protect your score

Track progress toward a good CIBIL

Improve credit score with timely insights

Improve approval chances for business loans

Manage debt smarter with score updates

Understand credit score range before applying

Unlock better interest rates with monitoring

What are the different credit score ranges and their meaning?

| Credit Score Range | What It Means | Impact on Borrowing |

|---|---|---|

| 300 – 549 | Poor credit score | High risk for lenders, loan approvals are unlikely. Immediate credit score improvement is needed. |

| 550 – 649 | Fair credit score | Limited chances of approval. It’s crucial to work on improving it. |

| 650 – 699 | Average credit score | Loans may be approved but at a higher interest rate. |

| 700 – 749 | Good credit score | Decent approval chances. Timely repayment helps in improving the credit score. |

| 750 – 900 | Excellent credit score | Strong financial health, high approval rate, and best loan terms. This is considered a good CIBIL score range in India. |

How to calculate credit score?

Credit bureaus use multiple factors to calculate your credit score. While the exact formula is not publicly shared, the following elements play a key role:

01

Repayment History (35%)

Timely payments on loans and credit cards strongly impact your CIBIL score. Even a single default can reduce your score.

02

Credit Utilization Ratio (30%)

Utilizing too much of your available credit can lower your score. Keeping credit card usage below 30% is advisable for a good credit score.

03

Length of Credit History (15%)

A longer credit history helps lenders trust your repayment habits. Regular credit score checks ensures you track this effectively.

04

Types of Credit Used (10%)

Maintaining a balanced combination of secured loans (such as mortgages) and unsecured loans (like personal loans) enhances your credit report.

05

New Credit Enquiries (10%)

Too many recent loan or card applications negatively affect your score. Before applying, always check your credit score to know where you stand.

Why having a good credit score is crucial

Easier access to loan approvals

Lower interest rates on loans

Higher credit card limits approved

Faster approval for online applications

Better chances of securing high-value loans

Improves chances of instant loan approval

Enhances overall financial credibility

Access to premium credit card offers

Why should I check my credit score?

Stay Loan-Ready Always

A regular credit score check ensures you know where you stand before applying for any loan or credit card.

Catch Errors Early

Reviewing your credit report helps identify mistakes that could pull down your CIBIL score unnecessarily.

Better Loan Approvals

Lenders look at your credit score online to decide approvals. A higher number means easier approvals and better terms.

Track Financial Growth

When you check your CIBIL score regularly, you see improvements as you manage repayments well—keeping your profile strong.

Free and Simple Process

You can get a free CIBIL score check done in just minutes.

Reasons for a low credit score

Missed or Late Payments

Consistently delaying EMIs or credit card payments negatively affects your credit score.

High Credit Utilization

Utilizing a large portion of your available credit reduces your CIBIL score.

Frequent Credit Applications

Multiple loan or card applications in a short span signal risk to lenders.

Errors in Credit Report

Incorrect entries in your credit report can lower your score unfairly.

Old Debts Unresolved

Unsettled loans or defaults from the past continue impacting your credit score.

Limited Credit History

Having very few loans or credit cards can make it hard to build a strong credit score.

How to increase credit score quickly?

1

Pay Bills On Time

Consistently paying EMIs, credit card bills, and other dues on time has a positive impact on your credit score.

2

Reduce Credit Utilization

Maintain credit usage below 30% of your available limit to improve your CIBIL score.

3

Avoid Frequent Loan Applications

Submitting too many applications for credit cards or loans in a short timeframe can lower your credit score.

4

Check and Correct Errors

Regularly review your CIBIL report and dispute any inaccuracies to avoid score dips.

5

Keep Old Accounts Active

Maintaining long-standing credit accounts helps build a stronger credit score range over time.

6

Diversify Credit Mix

A balanced combination of credit cards and loans can improve your credit score online and overall creditworthiness.

How credit score affects loan eligibility

Your credit score is essential in determining eligibility for loans and credit cards. A strong CIBIL score increases the chances of approval with favorable interest rates, while a low credit score can lead to higher rates of interest or possibly even a denial.

Lenders review your credit report to assess repayment behavior, outstanding debts, and credit utilization. Regular credit score check helps you stay informed and manage your financial health, ensuring smoother approvals for all types of loans.

List of credit information bureaus in India

CIBIL

(Credit Information Bureau India Limited)

The most widely used bureau, providing the popular CIBIL score.

CRIF High Mark

Offers credit reports and scores for individuals and businesses.

Equifax

Provides Equifax credit report solutions for individuals and lenders.

Experian India

Offers personal and business credit reports, scores, and risk assessment services.

What is a credit report?

A credit report is an extensive account of your financial behavior, showing how you manage loans, credit cards, and repayment history. It includes information like outstanding debts, credit inquiries, and repayment patterns. Lenders use your credit report to assess your reliability before approving a loan or credit card. Regularly checking your credit report helps you spot errors, monitor financial health, and maintain a good credit score. You can also perform a free CIBIL score check to ensure your report reflects accurate and up-to-date information.

What are the differences between a credit score, credit rating, and a credit report?

Why are credit reports important for businesses?

Credit reports are crucial for businesses as they provide a clear view of a company’s financial health and creditworthiness. Lenders and suppliers often rely on credit reports to decide on loans, credit limits, or partnerships. By reviewing credit reports regularly, businesses can identify potential risks, track outstanding debts, and ensure timely payments. Maintaining a good credit report helps secure favourable loan terms, build trust with partners, and support growth. For entrepreneurs and small businesses, checking their CIBIL report ensures informed financial decisions.

FrequentlyAsked Questions

Credit score is a 3-digit number usually between 300 and 900 . It is created using a complex statistical model that summarizes the past credit information of an individual. The number reflects the probability whether a borrower will pay off the loan in a timely fashion. A high number means you have been paying off your past dues (towards loans or credit cards) regularly and have rarely delayed payment. As a result, lenders have more confidence in extending credit to borrowers with high credit score.

Your credit score is only part of your credit report. Your credit report covers your entire history of dealing with credit (loans and credit cards) including your history of payments (on time or delayed). Your credit history would also show the current status of each credit account – active, closed, delinquent, settled etc. These as well as other details of your credit report form the basis of your credit score.

A high credit score is definitely an asset when it comes to loan and credit card applications. A high credit score (closer to 900) implies that you have good financial discipline and tend to pay off your dues on time. Thus, your chances of being approved for additional credit, in the form of a new loan or credit card, are higher. This is so because lenders perceive borrowers with high score as trustworthy. They notice the financial discipline of applicants and accordingly decide whether to extend new credit or not.

A credit inquiry is a request by an institution for Credit Report Information from a credit-reporting agency. They are classified as either a hard inquiry or a soft inquiry.

Hard inquiries (also known as ‘hard pulls’) generally occur when a financial institution, such as a lender or credit card issuer, checks your credit when making a lending decision. They commonly take place when you apply for a loan or a credit card.

Soft inquiries (also known as ‘soft pulls’) typically occur when a person or company checks your credit as part of a background check.

Your credit score is calculated taking into consideration several factors such as your credit history, repayment behavior, and credit type, among others.

These are the main factors that impact your credit score:

Payment History: Your payment history contains all the information about how you have maintained the credit in the past. Chances of loan approval get reduces if you are having any missing, delaying or incomplete payments over your credit card and loan EMIs as it affects your score negatively.

Credit utilization ratio: Credit utilization ratio is calculated as the ratio of your borrowed amount with your total available credit. Having the credit utilization ratio greater than 40% indicates the burden of increased repayment that can negatively affect your score.

Credit mix: Having a variety of loans is also one more factor lenders consider. Maintaining a balanced mix of secured loans and unsecured loans have a better positive impact on your credit score.

Credit Age: The age of your credit is calculated through the length of your credit history to check on how long you have been accessing credit. Having a longer experience in handling credit leads to better score.

Hard inquiries: The prospective lenders access your credit report whenever you have applied for credit card or a loan from the credit bureaus. It is reflected in your credit report as "hard inquiry". Hence, submitting multiple requests for credit within a short span has an adverse affect on your credit score.

Show More FAQs

Kissht - Sapno ko Kaho YES!

4.8

63M+

Downloads

5900Cr+

Assets Under Management

11M+

Customer Base